.svg)

Self-Employed in the UK (System View): What Newcomers Should Know in 2025–2026

A calm, information-only system view of self-employment in the UK in 2025–2026 — what “self-employed” means, how Self Assessment fits in, what timelines typically shape the process, and how Making Tax Digital rollout changes reporting for some taxpayers.

Clear, information-only updates on how key UK systems work — from healthcare and identity checks to everyday administrative steps.

No opinions. No advice. Just structured information to help you navigate your first stages in the UK with clarity and confidence.

Self-Employed in the UK (System View): What Newcomers Should Know in 2025–2026

Being “self-employed” in the UK is not a job title — it is a tax status used to describe income you earn for yourself (sole trader). It connects to Self Assessment, National Insurance, and (in some cases) Making Tax Digital.

This article is a calm, structured, information-only overview of how the system typically works in 2025–2026, based on publicly available HMRC guidance. It does not provide legal, immigration, financial, or tax advice.

1) What “Self-Employed” Means (System Definition)

In UK terms, “self-employed” usually means you operate as a sole trader (you trade in your own name or a business name, but you are personally responsible for the business).

It is different from:

- Employment (PAYE, employer runs payroll)

- Limited company director/shareholder (Companies House + corporation tax structure)

A person can also have mixed income (e.g., employment + self-employed).

2) The Core System Components You Will See

When self-employed income is relevant, the system usually includes:

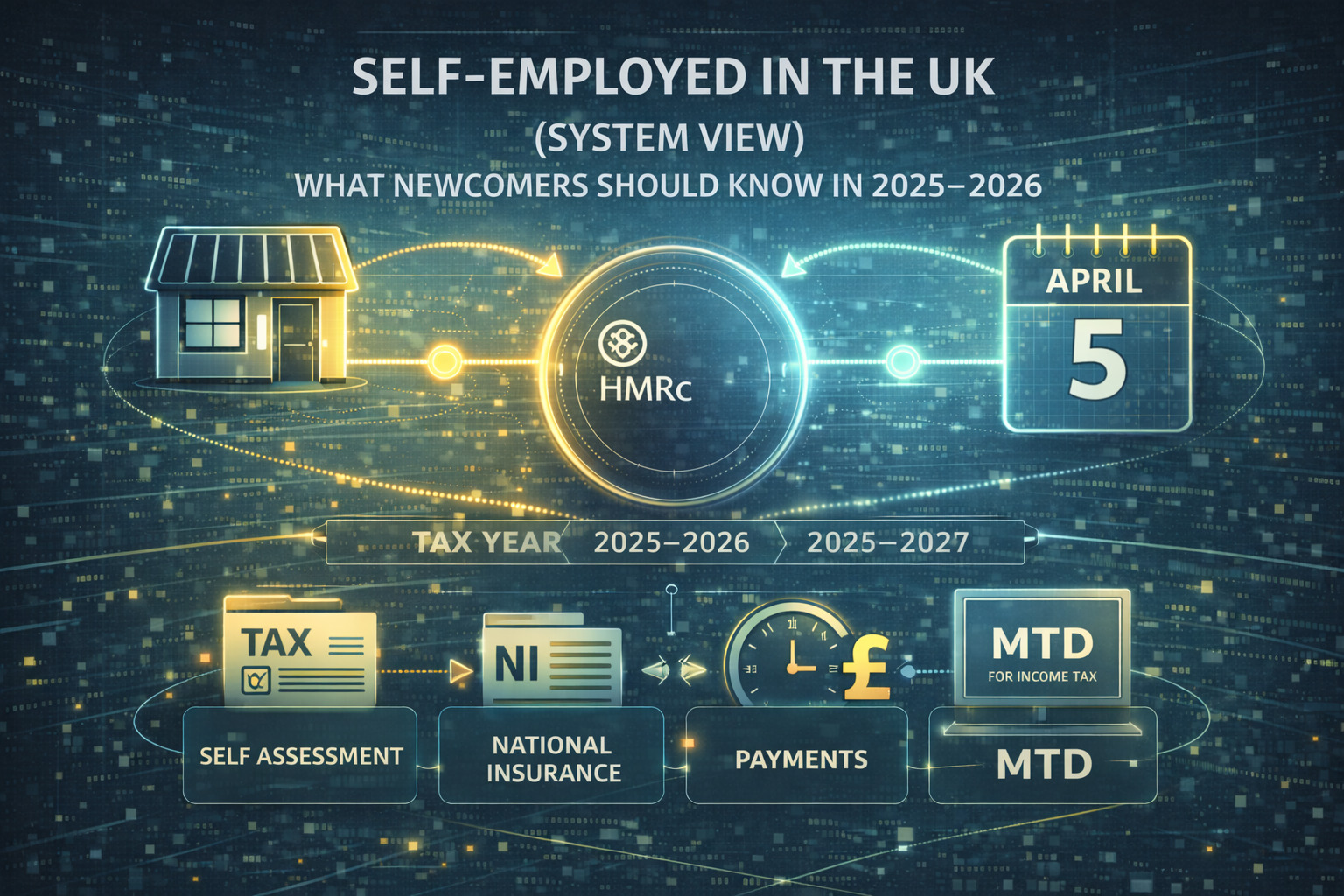

- Tax year logic (UK tax year runs 6 April to 5 April)

- Self Assessment (reporting income and calculating tax)

- National Insurance (rules depend on profit level and current thresholds)

- Records (evidence of income/expenses)

- Payments (often includes balancing payments and, for some people, payments on account)

HMRC provides tools to check whether a Self Assessment return is needed for a given tax year.

3) Typical Onboarding Flow (High-Level)

A structured “system view” of the usual flow looks like this:

- Start trading / earning self-employed income (sole trader activity begins)

- Tell HMRC / register for Self Assessment (for people who are new to Self Assessment)

- Receive a UTR (Unique Taxpayer Reference) if you need Self Assessment

- Keep records throughout the year (income and allowable expenses)

- Submit the tax return after the tax year ends

- Pay what is due by the relevant deadlines

If you are new to Self Assessment, HMRC reminders commonly reference 5 October (after the end of the relevant tax year) as a key “tell HMRC / register” date.

4) Key Dates That Shape the System

Even without going into “how to do it”, the system is shaped by a small set of recurring dates:

- Tax year: 6 April → 5 April

- Registration (new to Self Assessment): often referenced as by 5 October after the end of the tax year you started (typical HMRC reminder framing)

- Online filing and payment: commonly associated with 31 January deadlines (depending on your situation)

(Exact deadlines can differ by route and circumstances, so always confirm via HMRC guidance.)

5) Making Tax Digital (MTD) — The Rollout Newcomers Should Know

HMRC is moving some Self Assessment reporting into a “digital records + updates + software” model for certain taxpayers.

Making Tax Digital for Income Tax applies to sole traders and landlords above an income threshold. HMRC states that from 6 April 2026, those with qualifying income over £50,000 must use it.

Key implications (system-level):

- compatible software becomes part of the reporting process

- digital record-keeping is expected

- reporting may include periodic updates plus an end-of-year position (based on HMRC guidance)

MTD is a rollout area — thresholds, scope and onboarding steps are best verified on HMRC pages before acting.

6) Common Friction Points (Why People Get Stuck)

Newcomers usually experience delays due to system mismatches rather than “complexity”:

- mixing up self-employed vs limited company status

- inconsistent personal details across accounts (name/address)

- assuming “no tax owed” means “no reporting needed”

- missing records or unclear expense evidence

- misunderstanding which HMRC service (tool/account) is relevant

A calm check of “what system you’re in” usually resolves most confusion.

7) Practical Boundary: What This Article Does and Does Not Do

This guide explains system logic and typical flow. It does not:

- tell you what to claim or how to structure tax positions

- replace HMRC guidance or professional advice

- act on your behalf

If you need to understand how the parts connect (tax year → Self Assessment → payments → MTD), start with HMRC’s Self Assessment check tool and the MTD collection pages.

Final Thoughts

Self-employed in the UK is best understood as a system: a tax year structure, a reporting method, and (increasingly) a digital reporting rollout for some taxpayers. When you keep the definitions and timelines clear, the process becomes predictable.

If you want a calm overview of how your UK onboarding steps connect, you can request a Clarity Call — focused on structure and next steps, information-only.