.svg)

UK Tax Year: What Newcomers Should Know in 2025–2026

A structured, information-only overview of the UK tax year and why it matters for PAYE and Self Assessment. Includes the core 6 April–5 April timeline, common deadlines, typical misunderstandings, and a high-level note on HMRC’s staged digital reporting rollout from 2026 — without tax, legal, or financial advice.

Clear, information-only updates on how key UK systems work — from healthcare and identity checks to everyday administrative steps.

No opinions. No advice. Just structured information to help you navigate your first stages in the UK with clarity and confidence.

UK Tax Year: What Newcomers Should Know in 2025–2026

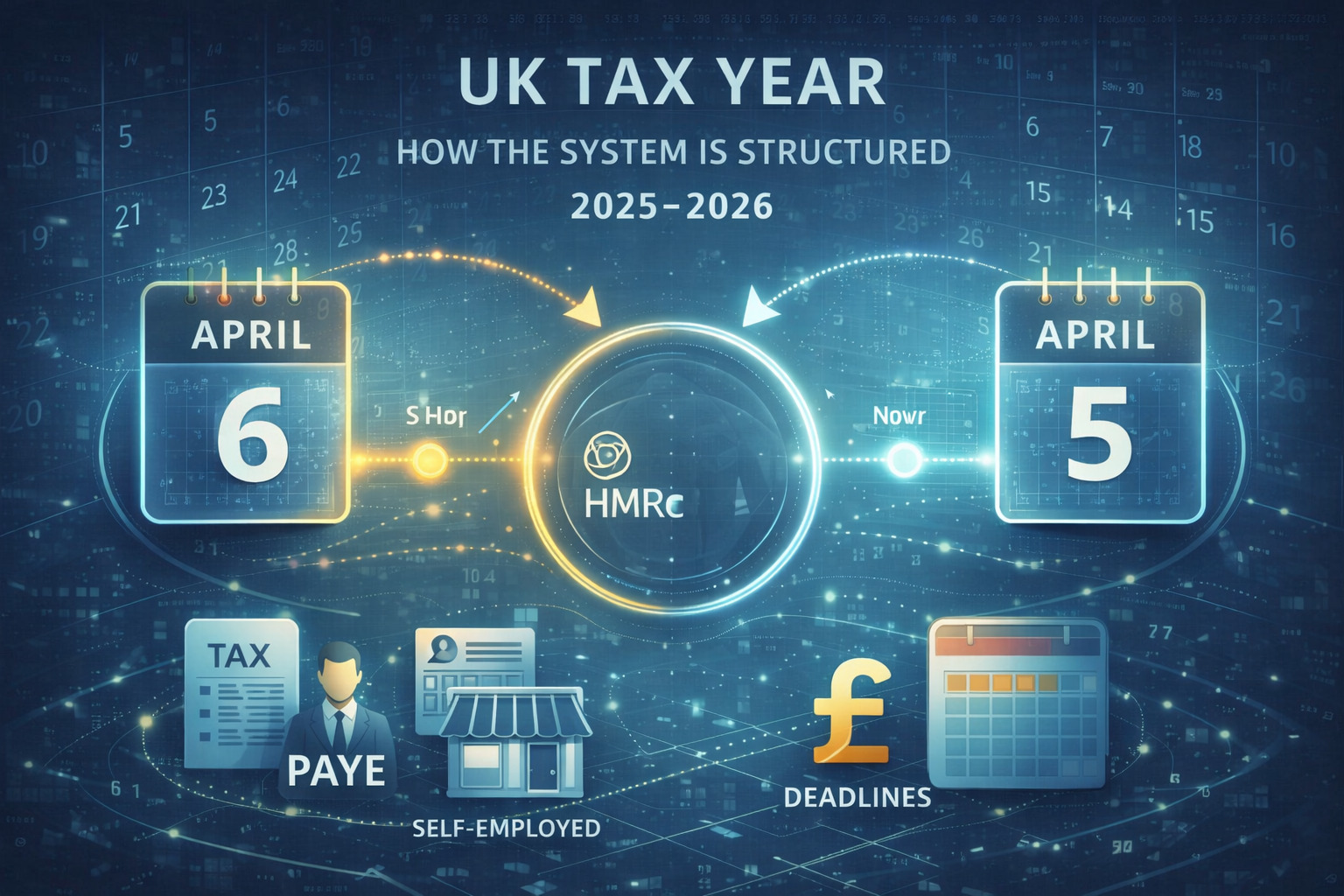

The UK tax year is not the same as the calendar year. It usually runs from 6 April to 5 April, and many HMRC timelines (PAYE records, Self Assessment, and upcoming digital reporting changes) are built around that structure.

This is a structured, information-only overview for newcomers. It does not provide tax, legal, or financial advice.

—

1) What the UK Tax Year is (and why it matters)

The tax year is the period HMRC uses to organise:

- income records (PAYE and other sources)

- National Insurance records

- Self Assessment returns (where relevant)

- tax calculations, allowances, and year-based reporting

A common point of confusion is thinking “tax year = January to December”. In the UK, it typically isn’t.

—

2) The core dates you will see in the UK system

Most people will repeatedly encounter:

- Tax year start: 6 April

- Tax year end: 5 April

- “Tax year 2025–2026” = 6 April 2025 to 5 April 2026 (the standard convention HMRC uses)

These dates are used across HMRC services and many employer payroll processes.

—

3) How the tax year connects to PAYE (employment)

If you work as an employee, your employer usually reports pay and tax through PAYE. In practice, that means:

- your pay is recorded against the UK tax year

- your tax code and deductions can change within the year

- HMRC summaries and annual views often follow the 6 April–5 April cycle

Many newcomers first notice the tax year when they compare payslips, P60/P45 timing, or HMRC account summaries.

—

4) How the tax year connects to Self Assessment (when it applies)

Not everyone needs Self Assessment. But if you do, the tax year affects:

- which period your return covers

- when filing and payment deadlines fall

Common (widely used) deadlines include:

- Paper return deadline: 31 October (after the tax year ends)

- Online return deadline: 31 January (after the tax year ends)

- Payment deadline (typical): 31 January (and sometimes 31 July for certain payments)

Deadlines can vary depending on your situation and notices from HMRC, so always cross-check the specific HMRC page or your HMRC account messages.

—

5) Practical examples (to remove calendar-year confusion)

- Income earned in May 2025 is in the 2025–2026 UK tax year.

- Income earned in February 2026 is still in the 2025–2026 UK tax year.

- Income earned in May 2026 is in the 2026–2027 UK tax year.

This structure is one reason UK admin often feels “offset” compared with many countries.

—

6) What’s changing: digital reporting (Making Tax Digital for Income Tax)

HMRC has confirmed a staged rollout of Making Tax Digital (MTD) for Income Tax, starting from April 2026 for relevant income levels, with further expansion in later years.

For newcomers, the key point is not the technical detail, but the system-level impact:

- more people may need to use compatible digital methods over time

- reporting may become more frequent/structured for those in scope

- the UK tax-year framework remains the organising backbone

Because rollout rules can change, treat any summary as directional and verify against the current GOV.UK guidance.

—

7) Common misunderstandings to avoid

Newcomers often get slowed down by:

- mixing up calendar year and UK tax year

- assuming “tax year” only matters if you are self-employed

- missing that some HMRC tasks and deadlines are after 5 April

- expecting one single “annual deadline” for everyone

A calm rule of thumb: first identify whether something is PAYE (employment) or Self Assessment (return-based), then map it to the tax year.

—

Final thoughts

Once you anchor everything to 6 April → 5 April, many UK timelines become predictable. The UK tax year is the shared reference point connecting PAYE, Self Assessment (when relevant), and the direction of future digital reporting.