.svg)

Income Reporting in the UK: How the System Works for Newcomers

An evergreen system-level overview of income reporting in the UK, explaining how tax year logic, income categories, HMRC records, Self Assessment and Making Tax Digital connect within the wider administrative system.

Clear, information-only updates on how key UK systems work — from healthcare and identity checks to everyday administrative steps.

No opinions. No advice. Just structured information to help you navigate your first stages in the UK with clarity and confidence.

Income Reporting in the UK

How the System Works for Newcomers

Income reporting in the United Kingdom is not a single form or one-time action.

It is a structured system built around the tax year, HMRC records, income categories, Self Assessment and, for some people, Making Tax Digital.

This article provides a calm, information-only explanation of how income reporting works at a system level.

It does not provide legal, financial, tax or immigration advice.

1. Income Reporting as a System

UK income reporting is based on several connected layers:

• the UK tax year

• income type

• HMRC records

• National Insurance records

• Self Assessment

• digital record-keeping requirements

The system does not treat all income in the same way.

Employment income, self-employed income, property income, dividends, savings interest and other income types may be reported through different routes.

2. The UK Tax Year

The UK tax year runs from 6 April to 5 April.

This date structure affects:

• when income is counted

• which tax year a record belongs to

• when Self Assessment may be needed

• when payments and deadlines apply

Understanding the tax year is the foundation of understanding income reporting.

3. Employment Income and PAYE

For employees, income is usually reported through PAYE.

In this structure:

• the employer reports pay to HMRC

• tax and National Insurance may be deducted through payroll

• HMRC receives regular payroll data

• the individual may not always need Self Assessment

PAYE is an employer-led reporting route.

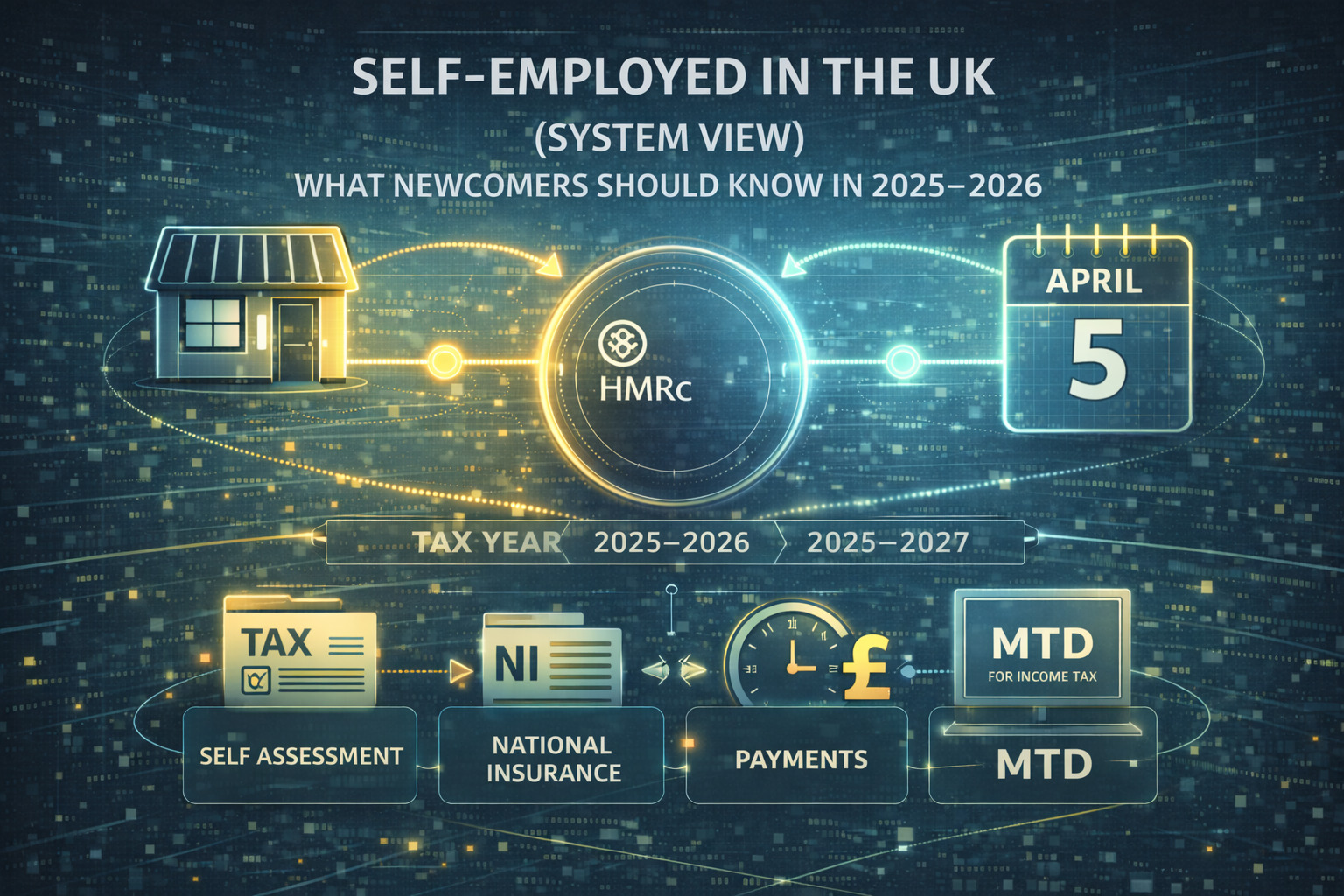

4. Self-Employed and Property Income

Self-employed income and property income usually sit closer to the Self Assessment system.

This may involve:

• keeping income and expense records

• reporting income after the tax year ends

• calculating tax and National Insurance where applicable

• paying any amount due by the relevant deadlines

For people new to Self Assessment, HMRC highlights 5 October after the relevant tax year as the date by which they must tell HMRC if they need to complete a tax return.

5. Self Assessment as a Reporting Framework

Self Assessment is not only a “tax return”.

It is a reporting framework used when HMRC needs information that is not fully captured automatically.

It may be relevant where income includes:

• self-employed activity

• property income

• untaxed income

• higher income situations

• certain foreign income

• other circumstances requiring direct reporting

HMRC provides an online tool to check whether a tax return may be needed.

6. Making Tax Digital for Income Tax

Making Tax Digital for Income Tax changes how some sole traders and landlords keep and submit records.

From 6 April 2026, Making Tax Digital applies to sole traders and landlords with qualifying income over £50,000.

The threshold is planned to reduce to £30,000 from 6 April 2027 and £20,000 from 6 April 2028.

This means that for affected people, income reporting becomes more digital and software-based.

The system may include:

• digital record keeping

• compatible software

• periodic updates

• end-of-year finalisation

MTD is a rollout area, so the applicable threshold and start date should always be checked against HMRC guidance.

7. Why Income Records Matter

Income records are used to support:

• tax calculation

• National Insurance records

• benefit or pension-related records

• credit and financial assessments

• business and self-employed evidence

• future administrative checks

Clear records reduce confusion when systems need to verify income history.

8. Common Points of Confusion

Newcomers often experience confusion around:

• the difference between income and profit

• PAYE vs Self Assessment

• sole trader vs limited company

• tax year vs calendar year

• HMRC registration vs tax return filing

• whether income is already reported automatically

Most confusion comes from overlapping systems, not from one single rule.

9. Timing and Deadlines

Income reporting is shaped by recurring timelines.

Common system dates include:

• 6 April - start of a new tax year

• 5 April - end of the tax year

• 5 October - telling HMRC if Self Assessment is needed in relevant cases

• 31 January - common online filing and payment deadline

The exact deadline depends on the reporting route and circumstances. HMRC confirms that online Self Assessment filing and payment are commonly linked to 31 January.

10. Why the System Feels Complex

Income reporting can feel complex because several systems operate at once:

• employer payroll

• HMRC tax records

• National Insurance records

• Self Assessment

• Making Tax Digital

• banking and financial evidence

• address and identity verification

The key is not to treat income reporting as one isolated task.

It is part of a wider administrative architecture.

Final Thoughts

Income reporting in the UK is best understood as a structured system.

The main layers are:

• tax year logic

• income type

• HMRC reporting route

• Self Assessment where relevant

• digital record-keeping for affected taxpayers

Clarity about these layers helps reduce uncertainty and makes the system easier to understand.